Passivated emitter rear cell (PERC) technology ascended to the solar throne in 2016 and became the dominant cell technology in only three years. According to statistics of the China Photovoltaic Industry Association (CPIA), all new installed solar cell lines in 2019 were PERC technology, and its market share grew to more than 65%. The conventional back surface field (BSF) solar cell retreated to slightly less than 32% globally compared to its 2017 share of over 83%.

It now appears that after years of continuous research and development, the efficiency improvement potential of PERC has been more or less exhausted. Scientific research has predicted the theoretical upper limit of PERC’s conversion efficiency is around 24.5%, and current mainstream products come to close 23% – with further improvements becoming difficult to achieve.

Even the largest PERC manufacturer, Longi Solar, has commented on the difficulty in achieving higher efficiencies with PERC without sharply increasing the marginal cost of production. Longi achieved 24.06% in R&D at end of 2019 and broke 23% in mass production in mid-2020.

Next-gen options

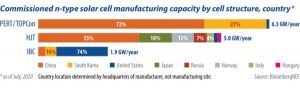

There are four main pathways for silicon cell technology beyond PERC: n-PERT (passivated emitter rear totally diffused), n-TOPCon (tunnel oxide passivated contact), heterojunction (HJT) and interdigitated back contact (IBC). None of these are new and all of them are being evaluated and optimized by R&D teams, institutions and business units the world over as candidates for the next mainstream solar cell technology. What unites them is that all are based on n-type silicon, rather than p-type.

Among all these four routes to the goal of higher efficiency, n-PERT and IBC appear to be out of the race, due to high costs, complicated manufacturing procedures and limited efficiency potential. This leaves TOPCon and HJT as contenders, and supporters of both are emerging, with each having its own set of advantages and pitfalls.

Key advantages

TOPCon technology originated with Germany’s Fraunhofer ISE, which went public with the approach in 2013. According to the institute’s research, and a later report at the Silicon PV 2019 conference, TOPCon is understood to have a theoretical efficiency ceiling of 28.2%-28.7%, beyond even the limit of HJT, which stands at 27.5%. The ceiling even approaches the theoretical limit of crystalline-silicon based solar cells at 29.43%.

More importantly, the production of TOPCon can utilize much of the equipment used in PERC lines, with the addition of two to three additional tools. This would significantly save on both time and money for the capacity investment, making TOPCon very attractive to those manufacturers currently operating PERC production lines.

In China, the current capital investment for TOPCon lines, per gigawatt of capacity, is still higher than for PERC, but reports are that it is declining as the required equipment is localized. Since 2019, several key equipment suppliers for TOPCon processes, including the LPCVD, PEALD and boron diffusion equipment, were successfully localized. This slashed the required investment to below CNY 350 million ($54.3 million) per gigawatt, encouraging manufacturers to join “team TOPCon.”

‘Team TOPCon’

Jolywood, the largest TOPCon player, had already installed and ramped up 2 GW of TOPCon cell lines at its Suzhou base by the end of 2020. Major integrated manufacturers – including heavyweight players such as Trina Solar, Canadian Solar, and Jinko – tend to embrace TOPCon. They have all invested significantly in R&D on TOPCon, installing pilot lines for further testing and making preparations for the coming shift. However, there are still obstacles in the way of TOPCon’s rapid expansion. Technical difficulties exist in the complex multistage process and result in low production yields. According to analysts at EnergyTrend, the average production yield of TOPCon lines they studied was around 93% – much lower than typical PERC yield of 97%-99%.

The TOPCon cell also requires significantly more silver than PERC in the metallization, around 130-150mg silver per piece, compared to 85mg with PERC – further pushing up cell costs. Another issue is the cost of human resources, which is higher for TOPCon, and difficult to reduce compared with HJT because of its complex nine or even ten production processes.

Despite these challenges, major PERC cell producers continue to develop TOPCon. Jinko for example, has publicly commented that “comparing TOPCon with HJT in several dimensions, we (Jinko) currently stand [for] TOPCon.”

At a conference in the solar stronghold of Wuxi in June 2020, Chen Yifeng – R&D vice director of high-efficiency solar cells at Trina Solar – said that “the HJT cell is revolutionary and totally different from previous lines, while TOPCon is evolutionary and compatible with most previous line equipment and saves costs.” Yifeng’s remarks were published on Chinese social media platform Xueqiu. He stated that he believes all the difficulties and problems currently attached to TOPCon will be solved gradually, with the combined effort of the entire industry – just like PERC before it.

HJT tech

Compared with TOPCon and other traditional solar cell technologies, HJT is quite a different beast. Perhaps by virtue of its uniqueness HJT has won many supporters.

production is considerably simpler than TOPCon, with far fewer steps. Compared to the seven manufacturing processes of PERC and nine to ten of TOPCon, HJT only needs four major process steps in total across the cell production line. Additionally, because of its technical features, HJT cells have a higher level of bifaciality – more than 90%.

Many features of HJT ameliorate the inherent defects of PERC. It exhibits better power performance in low light conditions, it is free of light induced degradation (LID) and potential induced degradation (PID) and exhibits a lower temperature coefficient.

HJT is also more compatible with thinner wafers and cells, with reduced thickness seen as a significant cost-reduction lever – particularly in times of rising polysilicon prices. HJT is also seen to be a good fit for combination with perovskites in tandem cells, which could deliver quite amazing conversion efficiencies, potentially of more than 30%.

All these factors have made HJT the new technology platform of choice, possessing the greatest potential for future development, and the best successor of PERC. For new entrants to PV manufacturing, and their financial backers attracted to the fast-growing PV market, HJT looks like the best option for entering the industry and also a rare opportunity to potentially overtake industry incumbents.

Since 2019, an increasing number of Chinese PV companies have taken the decision to enter the HJT field with pilot lines and some have announced mass production lines. As with TOPCon, these decisions were seemingly bolstered by reductions in HJT production costs due to production equipment localization, along with increasing conversion efficiencies.

Tongwei, a polysilicon supplier and major cell manufacturer, invested in two pilot HJT lines in 2019 and carried out further testing in 2020. At the end of 2020, Tongwei decided to build a HJT project with 1 GW of capacity for further testing and mass production. Canadian Solar and JA Solar all invested in pilot lines in 2020, with the latter recently announcing its intention to build two more lines in 2021. Risen, Akcome and state-owned Shanxi Coal Group are more aggressive and have already bet on gigawatt-scale HJT lines.

Like TOPCon, HJT too has challenges. HJT production may be simple in terms of process steps, but there are difficulties within these processes. Many aspects of each require careful optimization, costing both time and money. Another problem for HJT is silver costs, which can be three times higher than that of PERC due to the low temperature processing required at metalization. Special low-temperature silver paste must be used, and this material is currently largely monopolized by supplier Kyoto Electronics Manufacturing (KEM), meaning it comes at a high price. Equipment localization is still on its way and without more made-in-China HJT tools, the cost of HJT cannot compete with that of PERC.

Zhiyu Zhang, an experienced industry analyst who has worked for a securities advisory in the solar business, strongly favors HJT, and his logic is sound and simple. “HJT has many advantages over TOPCon, and all its shortcomings can be solved gradually with the development of technology,” Zhang said. “For instance, the difficult processes can be optimized, high silver cost will be cut down with substitution of local raw materials and improved high-precision welding process, and equipment localization will greatly reduce the cost to the level as TOPCon.”

End game

As to whether it will be TOPCon or HJT that emerges as the next king of solar cells, both have supporters and detractors. Indeed, the backing of leading industrial players will definitely provide a strong push for TOPCon. However, Zhang dissents from this opinion.“Just [because TOPCon is] supported by those giants doesn’t mean they are right and that TOPCon will win. Position determines action;” Zhang said. “They chose TOPCon only because they have to. And if the giants always win, we wouldn’t have seen mono beat multi, leading to the rise of PERC.”

The key to the competition between these two technologies is probably not which has more and stronger supporters, or which comes with more efficiency potential, but which technology can achieve the lowest production cost – or low enough to enable rapid deployment. Only with sufficiently low costs can any new technology overcome PERC and its massive market share.

In February, CPIA published a forecast of the future development of solar cell technologies. In it CPIA states that it sees TOPCon taking the lead in market share before 2024, after which point HJT will rise to the fore.